2024 Year-End Investment Considerations

Optimize your year-end investments with strategies for equity compensation, capital gains, diversification, tax planning, and more. Stay prepared for 2025!

Equity Compensation Inventory

Executives and professionals with equity compensation (RSUs/PSUs/ISOs/etc.) often find themselves with numerous grant types and positions over time. It’s critical to take inventory and have an organizational system in place to track all your grant information. This includes the award type, number of shares/options, grant date, vesting date, and more. Without good organization, you may lose track of your obligations, which can lead to poor decisions and unnecessary tax implications.

Also, create a thoughtful plan to manage your equity awards. What role do your equity awards play in meeting your financial goals? Will you hold/sell/exercise the grant upon the vesting date? How will you handle the taxes? How much company stock is too much? What is your strategy to reduce or exit the position in the future? As they say, failure to plan is planning to fail.

Capital Gains

If you own mutual funds in taxable accounts, be aware that December is usually when long-term capital gains are distributed. It is wise to check to see if the asset will distribute gains, the amount, and on what date.

If you own the asset and wish to avoid a potential capital gain distribution, you need to sell prior to the ex-dividend date, otherwise you will be subject to the distribution. Keep in mind that selling the asset may have additional tax implications.

If you are considering buying the asset, and you wish to avoid being subject to the distribution, you will need to buy it on or after the ex-dividend date.

Investment Allocation

Equity markets generally performed well in 2024, especially US markets. This may result in your investments now being overweight to Equities vs. Bonds, or perhaps overweight US equity vs. International/Emerging Markets.

For example, if your target allocation is 80% equity and 20% bonds, the rising equity market may have shifted your current allocation to something closer to 90%/10%. Check your allocation to make sure it is appropriate for your situation. Perhaps a rebalance is needed.

Tax-Smart Placement (Allocation)

Investors often have investment holdings across taxable, tax-deferred, and tax-free accounts. And each type of account has its own associated tax implications. Not only that, but the specific investments can be taxed differently. For example, interest from bonds is considered taxable income, while equities held longer than one year are taxed at capital gains rates.

Therefore, the tax-efficiency (or inefficiency) of the underlying investment strategy does matter. To minimize taxes and maximize after-tax returns, consider which investment strategy is placed (allocated) to each account type.

Because bonds are less tax efficient, it may make sense to place them inside tax-deferred accounts, such as a Traditional IRA. Low-turnover equity holdings and municipal bonds are better placed in taxable accounts. And high-turnover (tax-inefficient) equity holdings are better placed in tax-free accounts, like a Roth IRA.

Tax Harvesting

If you have investment losses in taxable accounts, those losses can be offset against investment gains. Short-term losses offset short-term gains, while long-term losses offset long-term gains. You may be in a situation where you have a highly appreciated asset in a taxable account. One way to reduce the gain is to sell another taxable position that has a loss.

Losses that exceed gains can be netted against ordinary income, but to a maximum of $3,000 per year (MFJ). Additional capital losses are then carried forward.

On the flip side, you may be in a low tax bracket this year, which presents an opportunity to sell assets in taxable accounts with capital gains and pay zero capital gains tax. In 2024, if you are married filing jointly and have taxable income below $94,050, the capital gains tax rate is 0%.

Global Diversification

According to Dimensional Fund Advisors, the global equity market consists of more than 15,000 publicly traded stocks spanning across 47 countries. As of 12/31/23, the US represented 61% of the world market capitalization, while International Developed Markets and Emerging Markets represented 26% and 12% respectively.

Similarly, the global investment grade bond market includes thousands of bond issuers and issues across 18+ countries. As of 12/31/23, the US represented 40% of this bond market.

This data is put forward to suggest that global diversification helps to reduce uncertainty, controls risk and increases the reliability of investment outcomes. Investing across and within global markets can broaden your investment universe and improve your investment profile.

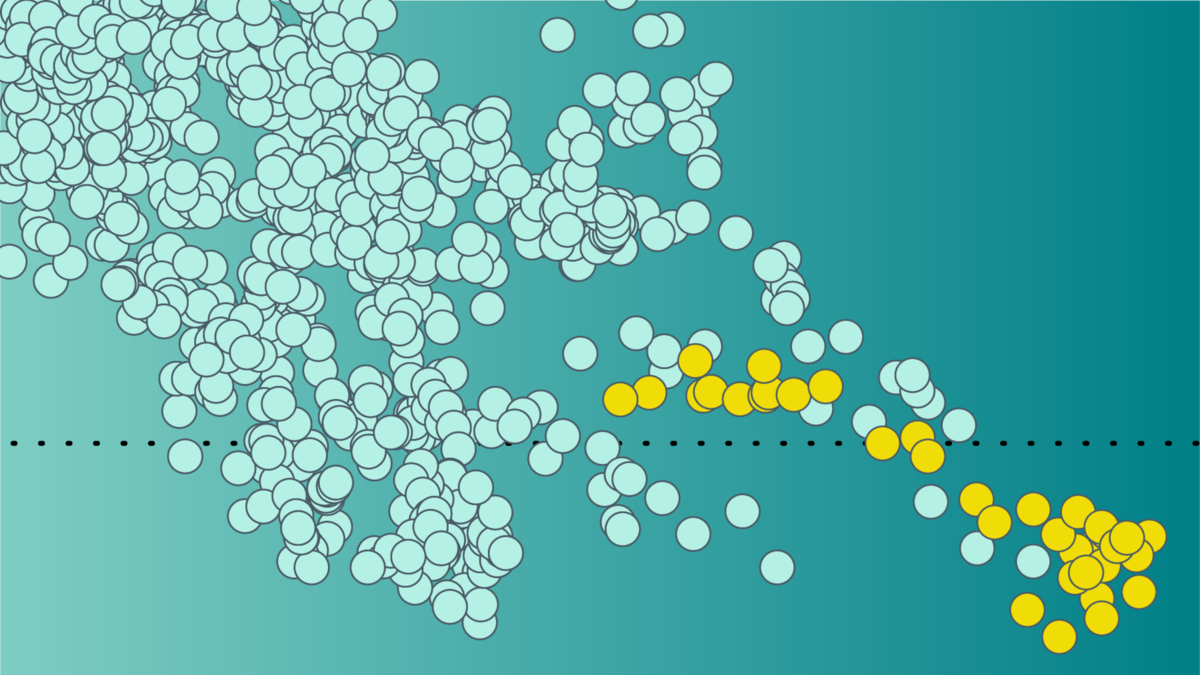

Concentrated Stock Positions

Executives with equity compensation often have a significant amount of company stock. This can build up over time and represent a substantial portion of your overall investment portfolio. Because you become so concentrated in a single stock position, it makes the portfolio top heavy and subject to unnecessary risk.

It is wise to assess your concentration risk and determine an appropriate level. Having a plan to cap your position weight and prudently trim the position can reduce risk and keep you on track for achieving your goals.

Gifting

Many executives and professionals are charitably inclined. They have generous hearts and use their financial resources to bless others. It is common for people to give cash donations to 501(c)(3) organizations especially during the holiday season.

Another consideration is to give away highly appreciated securities within taxable accounts. Perhaps you have accumulated a large stock position due to RSUs/PSUs. Or maybe you bought Apple or NVIDIA long ago, and now you have a big pile of stock with a low cost basis! Instead of donating cash, consider donating an equal value of your highly appreciated stock position to the charitable entity. Not only does this reduce your concentration risk, but it also provides a tax benefit. If you still wish to own the stock, now you can use the cash that you would have otherwise donated to acquire more stock shares with a higher cost basis.

HSA Holdings

If you have a Health Savings Account (HSA), how do you direct the contributions within the account? If you are using the HSA to pay for medical expenses, it makes sense to keep your contributions held in the cash position. However, if you are paying out of pocket for medical expenses and treating the HSA as a long-term investment vehicle, be sure to pay attention to how the contributions are being invested.

HSAs generally offer an extensive lineup of investment selections. Be sure to set up the HSA to invest your contributions in a way that is consistent with your financial goals. Because HSAs offer triple tax benefits, it is common to allocate towards investments with higher growth potential. Many people make the mistake of forgetting to invest the contributions and leaving everything in cash instead, which could result in years of lost investment opportunities.

Risk Level

Your risk level typically consists of your risk capacity (ability to take risk), risk perception, and risk attitude (tolerance).

As your financial, life, and career circumstances change throughout the year, it is a good idea to review your risk profile and determine if it still lines up with your goals. That does not necessarily imply an investment change, but it helps to monitor and document your risk profile over time.

Investment Fee Review

What are the fees and expense ratios on your investment holdings, such as mutual funds and ETFs? They do change over time, so it is smart to review the expenses periodically.

The good news is that expenses have come down significantly in the last 20 years. According to the 2023 Morningstar Annual US Fund Fee Study, the average fee has fallen from 0.87% in 2004 to 0.36% in 2023.

Summary

Investing is not a set-it-and-forget-it activity. Investing requires continuous planning, maintenance, and implementation. Changes in financial markets, the economy, politics, and in your personal life may impact your investment strategy. The considerations above can help you stay on top of your investments for the current year and get prepared for the coming year.

The foregoing content reflects the opinions of TwoTen Planning and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as financial, legal, tax, or investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. All investing involves risk, including the potential for loss of principal. There is no guarantee or assurance that diversification, strategies based on Nobel prize-winning research, or any investment plan or strategy will be successful. Consult an estate attorney or qualified tax professional for specific advice relating to those respective areas.

More Free Resources?

Sign up and receive our complimentary guide plus FREE regular updates!

Our Most Recent Blogs

Check out our most recent blogs where we share insightful articles, trends, and news from a Christ-centred perspective in the financial industry.

“For we are His workmanship, created in Christ Jesus for good works, which God prepared beforehand that we should walk in them.”